Key points:

- • Business sentiment remains stable, but confidence is softening and hiring plans are slowing.

- • Strong company performance contrasts with cautious consumer behavior and workforce challenges.

- • Declining confidence in local government and regulatory hurdles are emerging concerns.

April 2026 — Business sentiment across major U.S. metro areas held steady in the first quarter this year, but cracks are emerging as hiring plans are cooling and confidence in local government support is slipping, according to the latest Invest: Business Sentiment Survey (I:BSS).

April 2026 — Business sentiment across major U.S. metro areas held steady in the first quarter this year, but cracks are emerging as hiring plans are cooling and confidence in local government support is slipping, according to the latest Invest: Business Sentiment Survey (I:BSS).

Join us at caa’s upcoming leadership summits! These premier events bring together hundreds of public and private sector leaders to discuss the challenges and opportunities for businesses and investors. Find the next summit in a city near you!

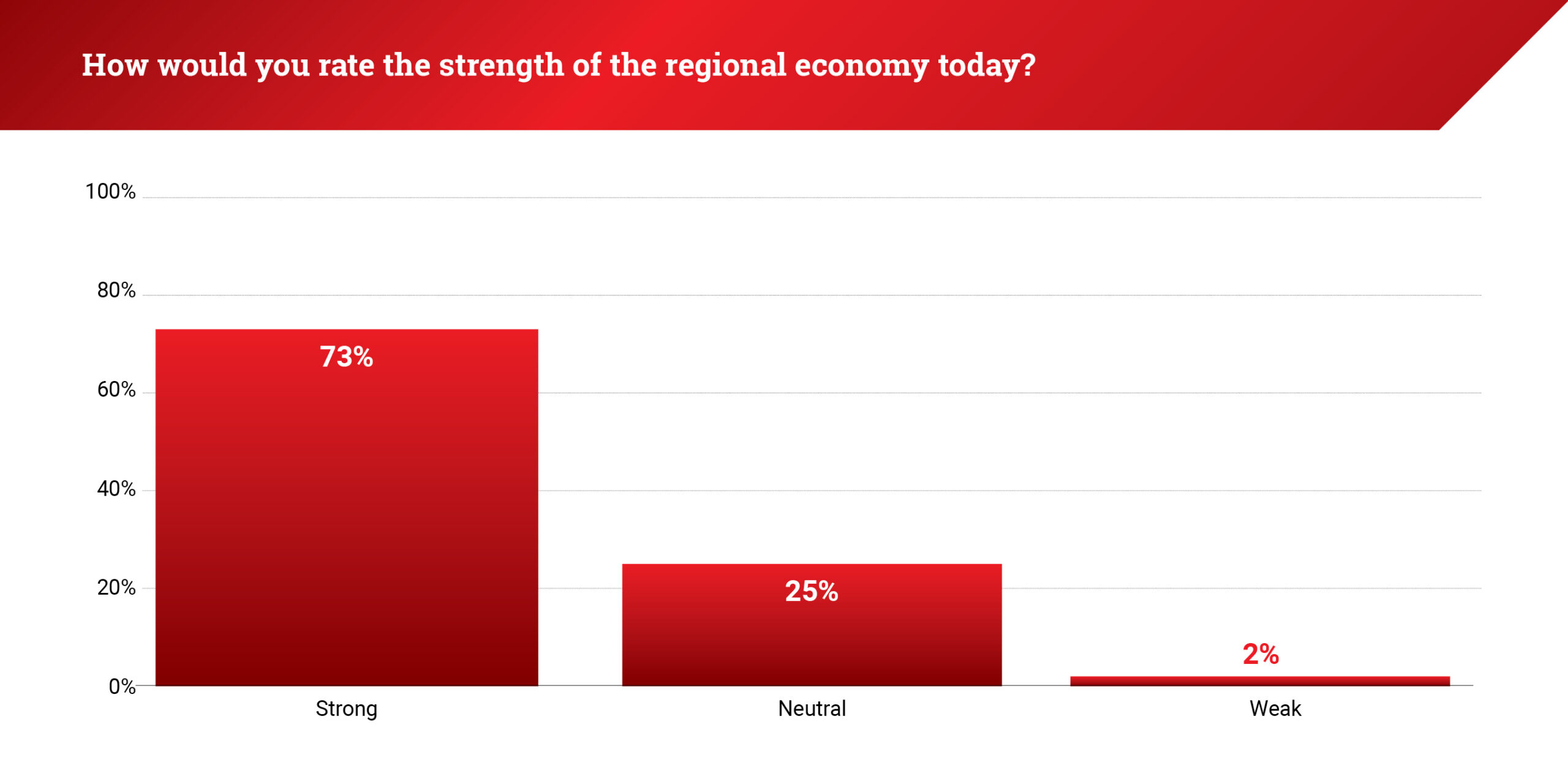

The score for regional economic sentiment dropped to 3.89 out of 5, down from 3.98 in the fourth quarter of 2025.

Some 73% of respondents rated their regional economy as strong, flat from last quarter but down from 78% a year ago.

“Client sentiment across most industries is positive… People continue moving here every day, which supports our clients, the broader economy, and both commercial and retail banking,” a banking leader in Charlotte shared with caa.

High-growth markets in the Southeast continue to benefit from population inflows and sustained demand.

“Florida is exceptionally well-positioned… The state remained open for business, attracted significant corporate relocations, and maintained economic momentum,” said a real estate executive in Orlando.

Energy-driven markets also continue to report steady activity.

“Houston continues to experience growth… Client demand remains strong, and business activity continues at a healthy pace,” an accounting leader in Houston said to caa.

Federal Reserve officials continue to describe the U.S. economy as resilient, supported by steady consumer spending and business investment, even as policy uncertainty and external shocks complicate the outlook.

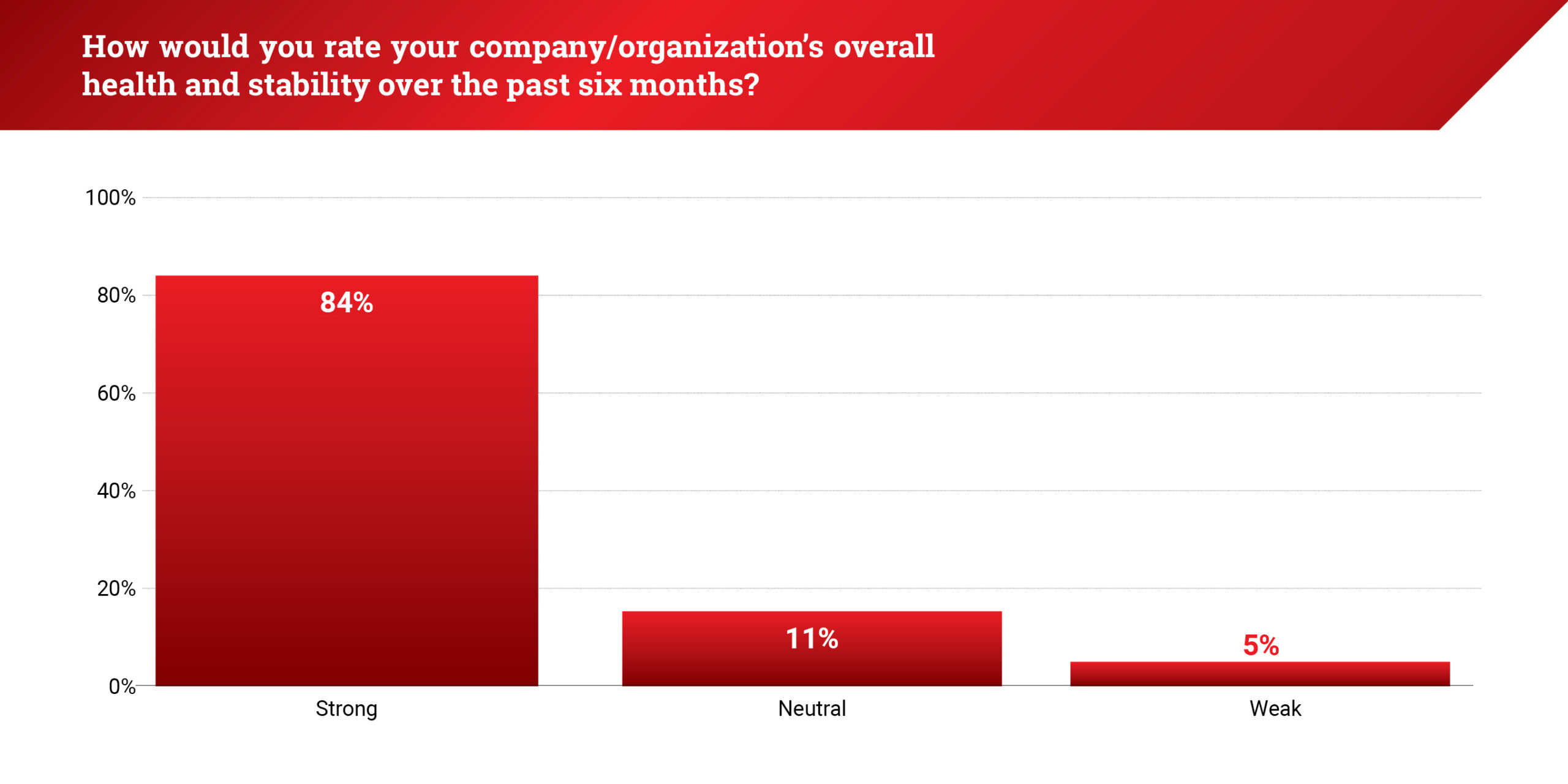

Company-level performance remained a bright spot: 90% of respondents rated their organization’s health and stability as strong over the past six months.

“We were able to grow our loan book substantially… expand certain segments of our commercial loan book, and continue identifying new, attractive, and profitable prospects,” a banking executive in Charlotte said.

Yet some executives are seeing consumers pull back.

“Demand remains strong… we are at 7.8% year-on-year growth… At the same time, families are more cautious,” an education leader in Houston said.

Recent commentary from the Federal Reserve points to a gradual cooling in hiring activity, as businesses adjust to higher financing costs and slower growth expectations, even as layoffs remain contained and overall labor market conditions stabilize.

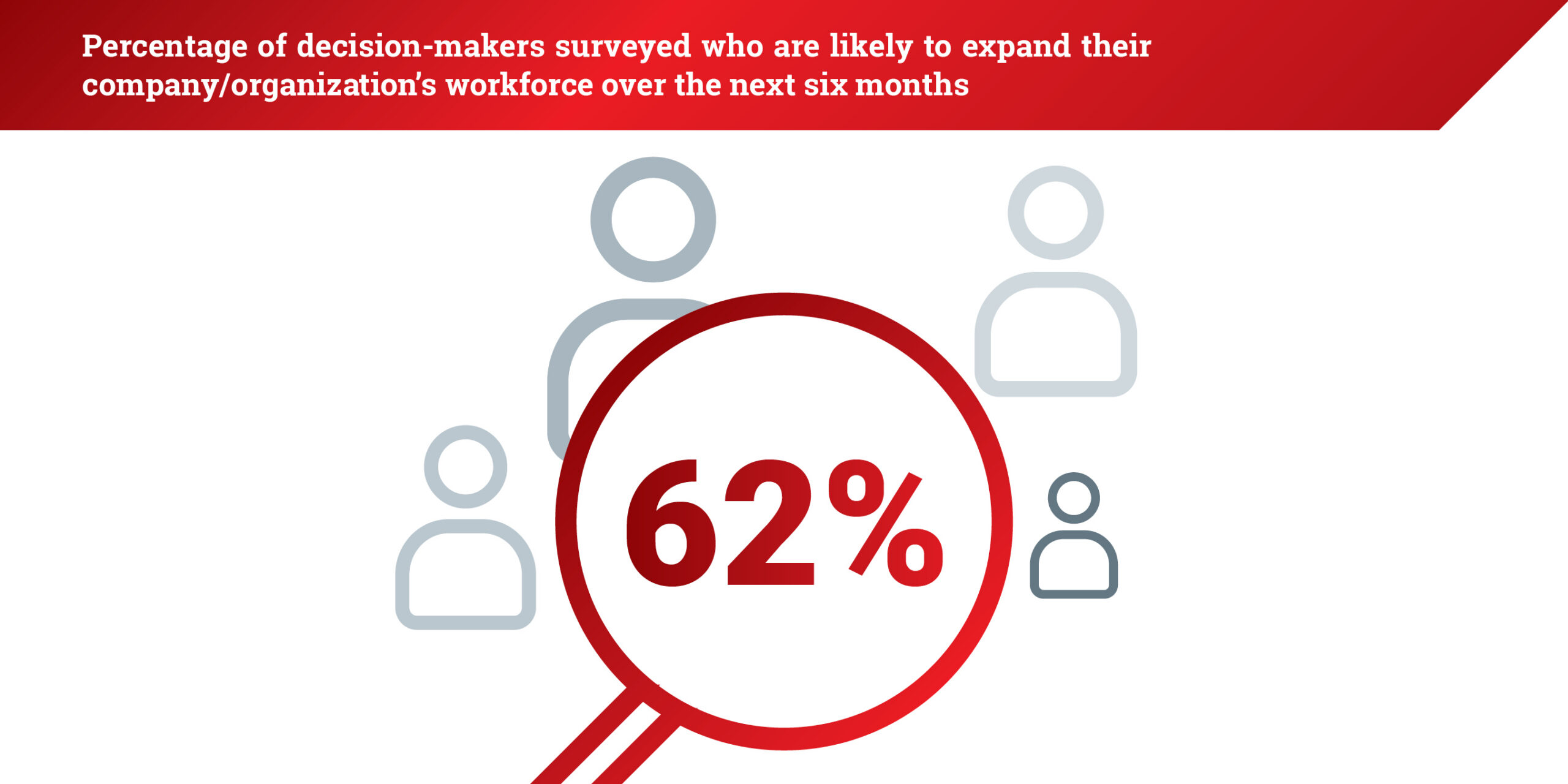

Hiring appetite is fading. Just 69% of respondents plan to expand their workforce in the next six months, down from prior quarters.

“Labor is one of the biggest challenges… Identifying and attracting the right talent has become even more complex,” a real estate executive in Orlando said.

Structural shifts in workforce expectations are also reshaping hiring strategies. Researchers at the Stanford Institute for Economic Policy Research call it a “low-hire, low-fire” equilibrium, with job levels stable but fewer being created. Through the first three months of 2026, the U.S. unemployment rate has hovered between 4.3% and 4.4%.

“The accounting profession is experiencing both retirements and workforce shifts… professionals value flexibility more than ever,” an accounting executive in Houston told caa.

“The speed of change fundamentally shifts how people think about their careers… we must train people for what the workforce demands now,” a technology leader in the Triangle market said.

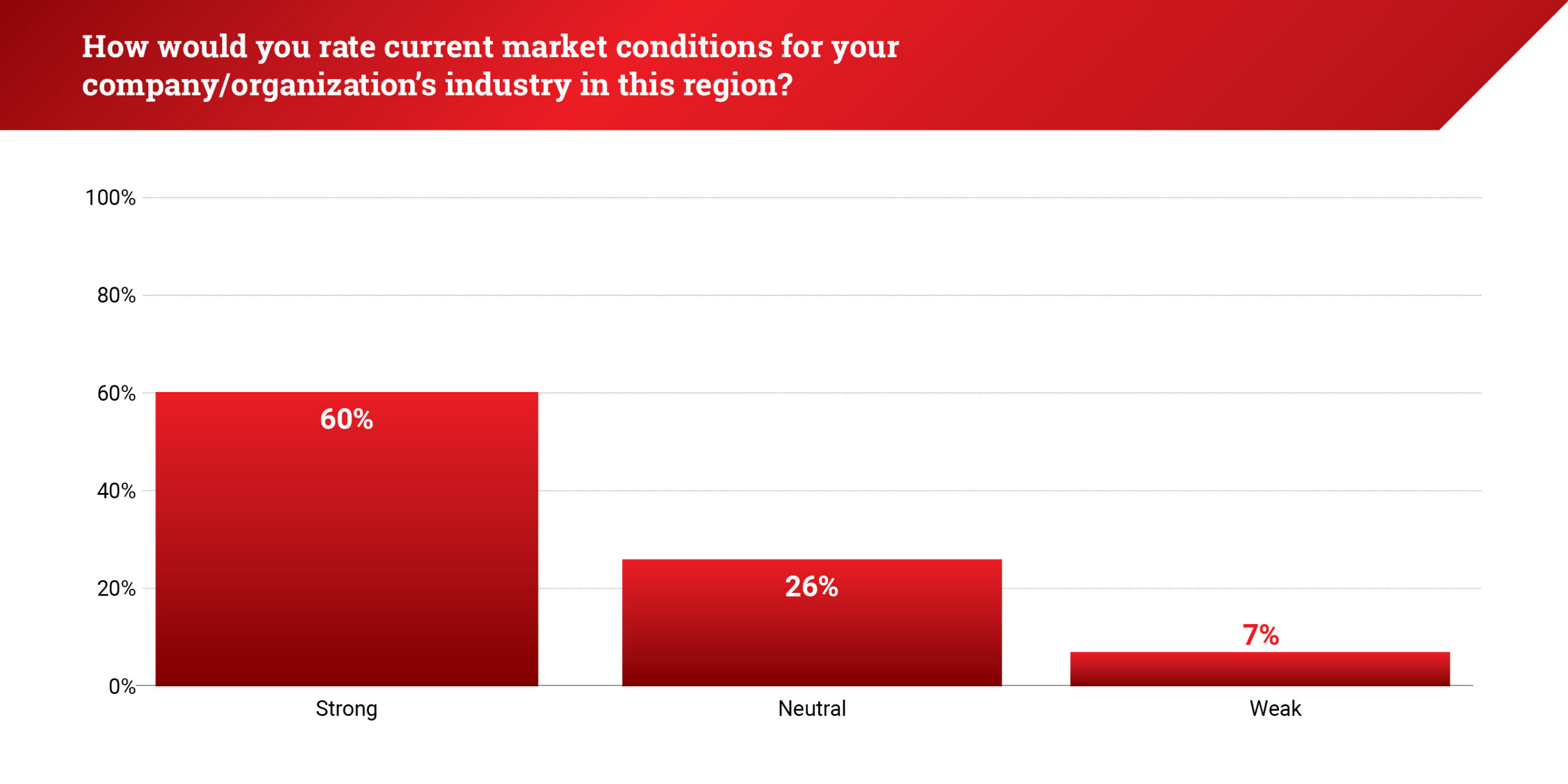

Market conditions held steady. Sixty-seven percent of respondents rated current industry conditions as strong, 26% as neutral, and 7% as weak, consistent with prior survey results.

“Inflation is tangible… business owners feel it in labor, materials, and supply chains… tariffs and increased sourcing costs are forcing price adjustments,” an accounting leader in Houston shared with caa.

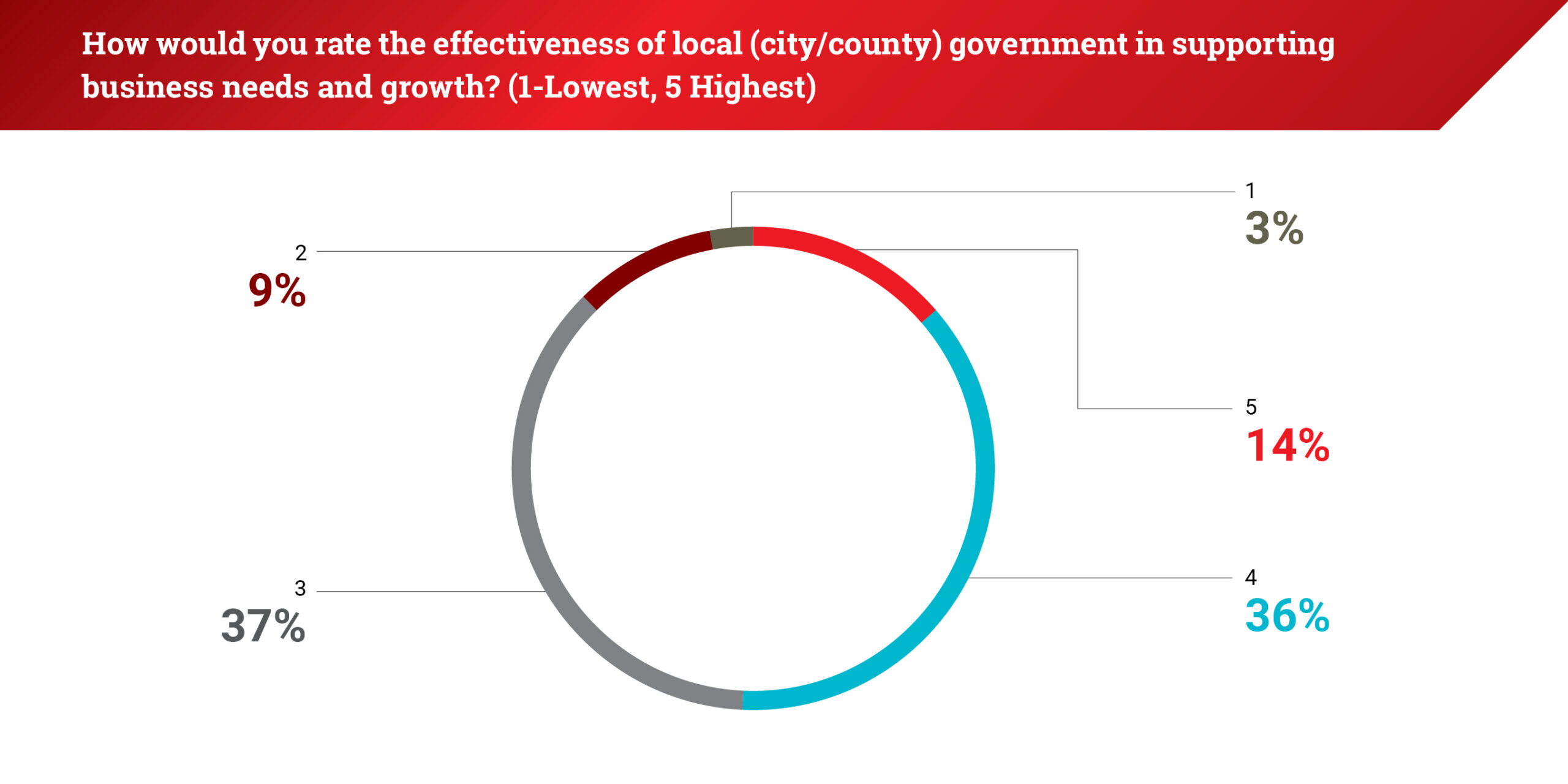

Views on local government support split sharply. Fifty percent of respondents rated government effectiveness as strong (scores of 4 or 5), though sentiment declined slightly from the previous quarter and varied across regions.

“We’ve made changes that allow small businesses to upgrade facilities more efficiently… that saves time and money,” a government leader in the Fort Lauderdale market said.

However, leaders continue to point to permitting and regulatory processes as areas for improvement.

“Streamlining permitting and development processes is one way local governments can help,” another public-sector leader in the Fort Lauderdale market shared with caa.

For more I:BSS reports, click here.

Alberto Guzman, Partner & Managing Director, AbitOs

Alberto Guzman, Partner & Managing Director, AbitOs Mike Morroni, President of Global Expansion, H&CO

Mike Morroni, President of Global Expansion, H&CO Ryan Morris, Partner, Sheppard Morris CPA

Ryan Morris, Partner, Sheppard Morris CPA Curt Edwards, Managing Director of Wealth Management – Southeast Region, Wilmington Trust

Curt Edwards, Managing Director of Wealth Management – Southeast Region, Wilmington Trust

Mike Blake, Mayor, City of Cocoa

Mike Blake, Mayor, City of Cocoa

Invest: sat down with Jerry Demings, mayor of

Invest: sat down with Jerry Demings, mayor of

April 2026 — Invest: spoke with Alexander Esposito, co-founder and CEO of

April 2026 — Invest: spoke with Alexander Esposito, co-founder and CEO of

April 2026 — Invest:

April 2026 — Invest:

April 2026 — Invest: spoke with Mario Fujii, president and CEO of

April 2026 — Invest: spoke with Mario Fujii, president and CEO of

April 2026 — Invest: spoke with Rob Shaw, CEO of

April 2026 — Invest: spoke with Rob Shaw, CEO of