Writer: Ryan Gandolfo

July 2024 – Business leaders maintained a generally positive outlook for their companies and regional economies in the Northern and Southern United States, according to the latest Capital Analytics Business Sentiment Survey (CABSS), conducted in the second quarter ended in June.

July 2024 – Business leaders maintained a generally positive outlook for their companies and regional economies in the Northern and Southern United States, according to the latest Capital Analytics Business Sentiment Survey (CABSS), conducted in the second quarter ended in June.

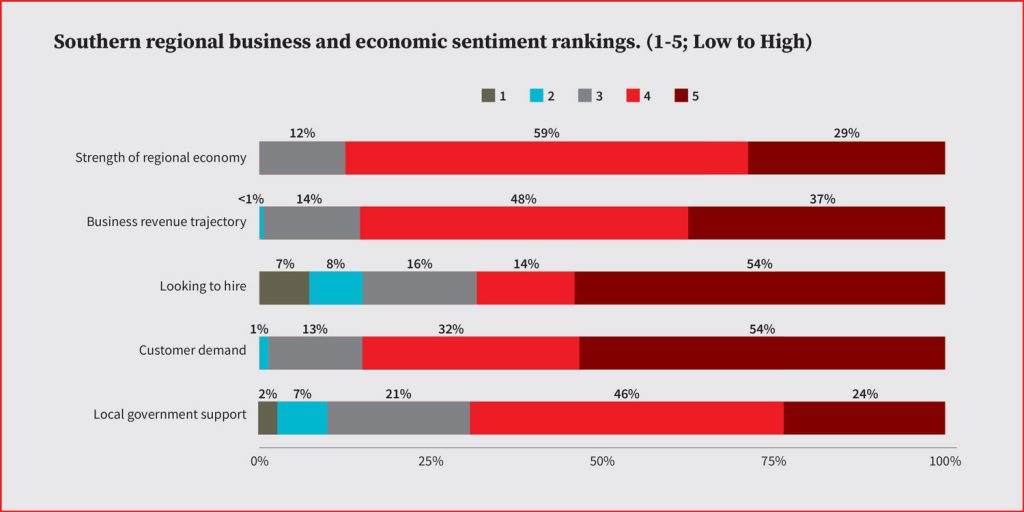

In survey responses from more than 300 public and private sector leaders in markets covered by Capital Analytics’ annual economic reports, from April 2024 through June 2024, market leaders ranked the strength of their regional economy 4.08 out of 5 (5 being the highest), on average. The new figure represents a 1% increase from the previous quarter, indicating steady sentiment, as business leaders continue to monitor the Federal Reserve’s actions regarding interest rates.

Southern market leaders held more favorable views in the quarter, with 88% of respondents ranking their area economy 4 or 5, while 63% of Northern market leaders shared the same positive sentiment. Both indicators show improving sentiment in consecutive quarters, but inflation continues to linger right above the Fed’s 2% target, and uncertainty around rate moves remains unabated.

“You cannot mention today’s economy without talking about interest rates, inflation, or other huge factors that are otherwise linked to one another. There is no secret here that our clients are pivoting due to the change in interest rates,” a Tennessee market leader in the construction sector told Capital Analytics.

“It is remarkable that this has not slowed things down more. It is a bit of a mixed bag. There has been quite a bit of impact, especially on the commercial sector when coupled with the lower office occupancy rates and the interest rate issue. We have seen pretty strong continued growth in Middle Tennessee. We are still setting records for construction permitting, but we have seen a bit of a downturn in construction volume for the first time in many years. There are mixed signals, but overall there is some caution due to interest rates,” he added.

The majority of Northern leaders who participated in the CABSS 2Q24 survey expressed a positive viewpoint regarding the current strength of their regional economy, with 63% ranking their area economies 4 or 5 — a 2% increase from last quarter and up 7% year-over-year.

In terms of business revenue trajectory, both Northern and Southern market leaders expressed overall positive sentiment, with 85% and 86%, respectively, ranking projected revenues in the coming six months at 4 or higher. While still high, overall sentiment for the Northern market revenue trajectory fell 11% compared to 1Q24.

“Just like any business, we are trying to increase revenue. As a law firm, we do this by increasing headcount and productivity. This office roughly doubled in size in the past year and did close to the same in revenue,” a Carolinas-based law firm managing partner told Capital Analytics.

According to the Second Quarter 2024 Survey of Professional Forecasters, the near-term outlook for the U.S. economy also looks better compared to earlier this year, with forecasters predicting national gross domestic product (GDP) to expand 2.1% in 2Q24, up from earlier expectations of 1.5%.

On the labor front, the majority of decision-makers are still looking to hire but at a lower level than the previous quarter. Nearly 7 in 10 (70%) survey respondents in Southern markets rank hiring expectations over the next six months at 4 or higher, compared to 72% in Northern markets.

Demand for products and services in both Northern and Southern markets continues to be strong, with 86% of respondents ranking their demand at 4 or higher. For colleges, unique programs that give students greater access to the workplace have led to a rise in enrollment.

“We’re seeing an increase in enrollment, which I’m happy to share. Several factors contribute to this, including our hands-on experiential education and co-op program. This program provides real-world experience for graduates, many of whom transition directly from their co-op assignments to full-time jobs with their co-op employers. This smooth transition into the workplace is a significant advantage,” a Massachusetts higher education president told Capital Analytics.

On local government support, market leaders wavered on optimism. While the majority of respondents (68%) in Southern markets selected 4 or higher, Northern market leaders were less enthusiastic with 39% providing a positive score.

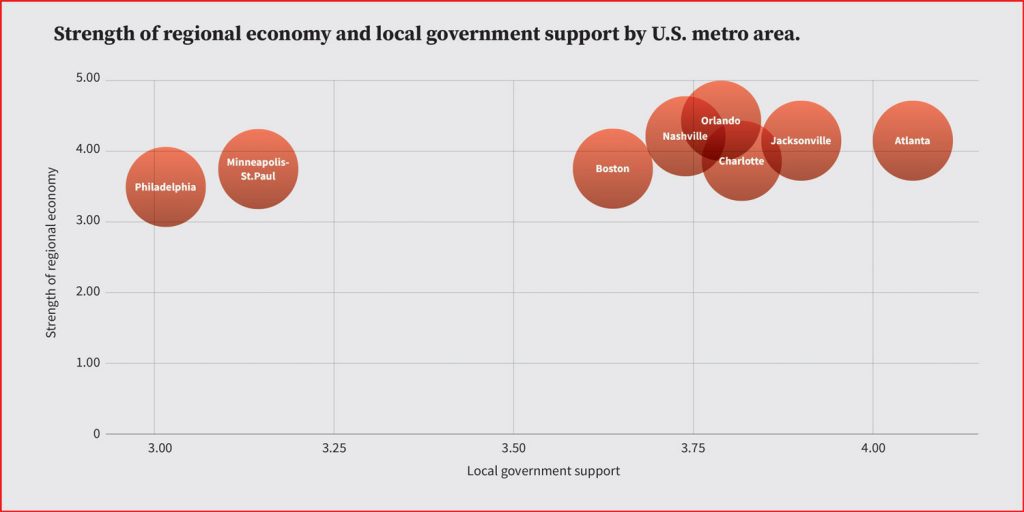

Across the markets covered at CAA, overall business and economic sentiment remains high, with Southern metro areas reporting slightly higher ratings for both the strength of their regional economy and local government support.

For an in-depth analysis of CABSS 2Q24 findings, read our Northern and Southern reports.